IMPORT TARIFFS - LATEST NEWS & UPDATES

Between estimating duties and finding the right U.S. Harmonized Tariff System (HTS) code to classify your imports, it should come as no surprise mistakes can happen in documentation. CBP realizes this and has mechanisms in place to correct errors before penalties can ensue. Post summary correction (PSC) is one such mechanism, and our brokers have years of experience submitting these corrections on behalf of importers.

Key Takeaways

Knowing when to use a PSC can prevent issues with CBP before they occur. Let’s explore how.

Don’t waste your valuable time and resources struggling with customs on your own. Let our importing specialists take that burden off your shoulders.

CBP’s post-summary correction process allows importers in the US to make corrections to the 7501 entry summary form prior to the CBP liquidation process. They’re used when an importer or broker makes a mistake filling out certain data points on this form.

When a post summary correction is submitted to CBP, it basically acts as a new summary, requiring payment prior to processing. Entries that have already been liquidated are not eligible for this process.

While not every entry type can be amended via PSC, many types commonly used by commercial importers can.

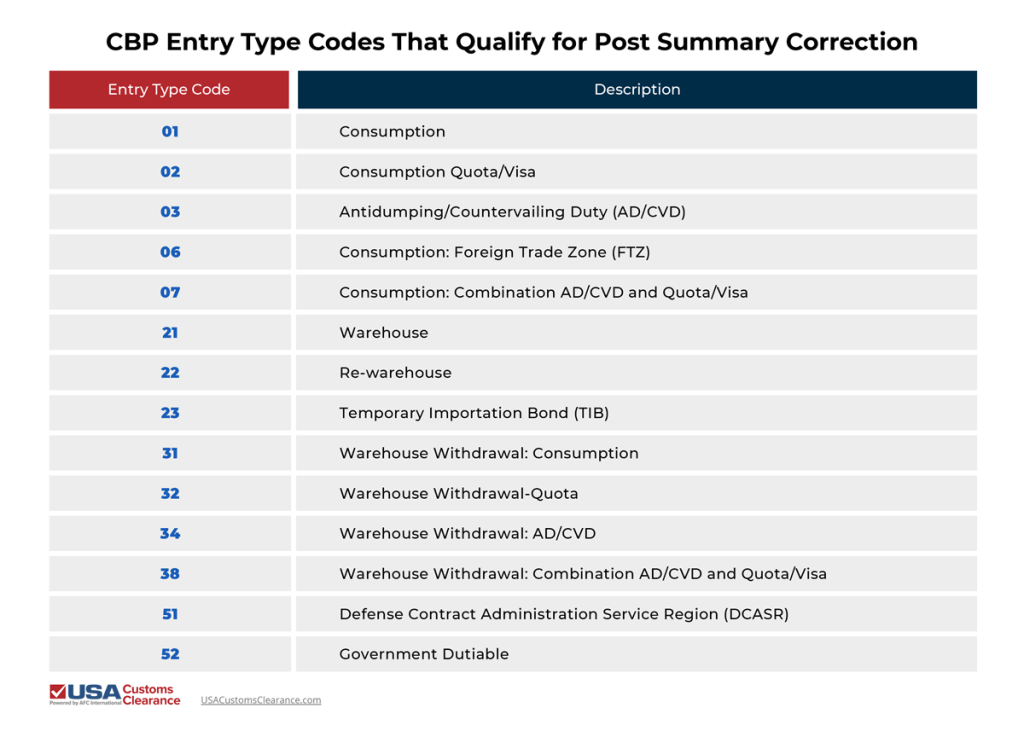

One of the first criteria you should use to determine if your goods qualify for a post summary correction is the entry type. CBP allows PSCs for the following 14 types of entries.

It’s important to distinguish that while these entry types can have their information corrected via a PSC, the entry type itself can only be changed if you’re going from 01 to 03 or vice versa.

Outside of these entries, you won’t be able to correct documents and submissions via a PSC, and not all data points on the entry summary can be corrected this way regardless of entry type. That said, they can be used to correct many common mistakes made by commercial importers.

Related: US Import Duties: Find Rates, Calculate Costs, and Pay CBP

The main reason to submit a PSC is to correct erroneous data on an entry summary. This is a legal obligation explained in Title 19 of the Code of Federal Regulations.

Some examples of data fields that can be amended using this process are:

Finding and correcting these errors before CBP liquidation can keep you from paying fines later if the government audits your import transactions. Filing a PSC requires Automated Broker Interface (ABI) software and access to CBP’s Automated Commercial Environment (ACE) portal, which means a broker must usually submit the PSC on behalf of the importer of record (IOR).

Our personalized approach and commitment to customer service will help you understand your unique customs needs.

Importers use tariff and duty rates to estimate the import taxes they will owe to CBP and rely on their export partners to provide invoices that accurately reflect the quantity and types of merchandise being shipped.

In the following scenarios, you’ll see how a PSC is used to make changes to the entry summary that can prevent punitive actions from CBP.

An auto parts manufacturer orders a number of machining components from a supplier in Germany to make custom exhaust parts from imported steel and aluminum materials such as pipes. The components are valued at $100,000 on the entry summary. The shipment is cleared, released, and brought to the manufacturer.

However, a compliance audit three months later reveals that before the components were built, the auto parts manufacturer paid the same supplier in Germany $10,000 to develop the initial engineering drawings for them. This first transaction qualifies as a dutiable assist, increasing the declared value of the shipment.

Since the shipment still hasn’t been liquidated by CBP, the importer can submit a PSC to accurately reflect the increased value of the shipment and pay whatever duties and additional fees are due after recalculation. Doing so lets the importer avoid potential fines that could come from a CBP audit.

An ecommerce business imports a shipment of toy flutes intended for children between 3 and 12 years of age. On the entry summary, they classify the goods under HTS code 9205.90.60 as flutes. This classification carries a 4.9% ad valorem duty.

This turns out to be a mistake as an import audit later shows that instruments which can be classified as toys fall under a different chapter of the HTS. The toy flutes should have been imported under a chapter 95 code indicating toys for children aged 3 to 12 years. Such goods have a free general rate of duty.

By submitting a PSC prior to liquidation, the business is able to correct this error and eventually pursue a refund for the overpaid duties due to misclassification.

Speaking of refunding duties, a PSC is just one of a few avenues that can eventually lead to a drawback, and some importers conflate corrections with another option: protests.

While a PSC can be submitted to correct information within the previously mentioned time window, filing a protest differs significantly in the following two ways:

There are some situations that will require you to file a protest even if you’ve already filed a PSC. Chiefly, if liquidation occurs while the PSC is still under review, the correction will be considered void and you will need to use the CBP protest process instead. Timing plays an important hand in the acceptance or refusal of your summary correction.

Related: CBP Clearance Process: A Guide for Importers

As the earlier scenarios illustrated, a post summary correction often starts during an internal compliance audit or transactional audit. Once a mistake has been found, there are some important timelines within which you’ll need to work during the PSC process.

The PSC must be filed within the earlier of the following two dates: 300 days from your shipment’s entry date or within 15 days of its scheduled liquidation by CBP. Exceptions to the 300 day rule can be made if the importer successfully files a liquidation extension, but the filing still must be made 15 days or more prior to the new date.

There are also exceptions for entry types 03, 07, and 06 if your cargo received a suspended status due to AD/CVD regulations.

Since submitting a post summary correction requires expensive software that many importers don’t have or can’t access, they usually rely on licensed customs brokers to make the actual filing with CBP.

If you have an entry in need of correction, call us at (855) 912-0406 or fill out a contact form online to get started avoiding costly repercussions.

Copy URL to Clipboard

Copy URL to Clipboard

Add usacustomsclearance.com as a preferred source!

See more of our coverage in Google's Top Stories.

Add usacustomclearance.com as a preferred source!

See more of our coverage in Google's Top Stories.

Add your first comment to this post